The Other 2.6 Billion

The next platforms will emerge where the last billions of people meet the next billions of devices.

[6 min read]

Philip Mordecai, Florido Consulting

Last month, we witnessed remarkable new frontier stories emerging from the seasonal tech events such as Mobile World Congress in Barcelona and NVIDIA GTC in sunny San Jose. The exhibition floor was crowded with AI-native networks, hybrid satellite-to-anywhere connectivity and early 6G demonstrations promising yet another leap in speed of our LLM experiences.

It’s impressive, but it also obscures a more uncomfortable reality: while we optimise for the next smartwatch, device and gigabit, billions of people still aren’t connected at all.

This piece is about that frontier. We’ll look at how the next wave of opportunity, platforms and SME growth can turn the remaining billions of people (and billions more devices) from “unreachable” into the next generation of participants in the networked economy. For the past decade, most conversations about the future of technology have centred on cloud, SaaS and artificial intelligence. New models, new assistants, new tools, each wave promising to automate another category of work and reshape how organisations operate.

But beneath the noise sits a quieter reality that matters just as much for SME leaders, founders, boards and investors trying to understand where the next wave of opportunity will come from. The internet itself is still not finished expanding.

“Believe it or not, the internet is still in rollout mode”

— Philip Mordecai, Florido

According to the Digital 2025 global report from We Are Social, the world’s population now stands at 8.20 billion people, of which 5.56 billion are internet users. That leaves 2.63 billion people still offline today. The International Telecommunication Union (ITU) reports a similar figure, estimating that 2.6 billion people globally remain unconnected. That means roughly one in three people on the planet is still outside the digital economy.

Source: WE ARE SOCIAL - Digital 2025 April Global Statshot Report

Those who are already connected are interacting with the internet in very different ways than they did a decade ago. We Are Social estimates there are now 5.78 billion mobile phone users globally, with smartphones accounting for the vast majority of active handsets. Connectivity is no longer centred on a single device; it is distributed across pockets, homes, cars, workplaces and city streets.

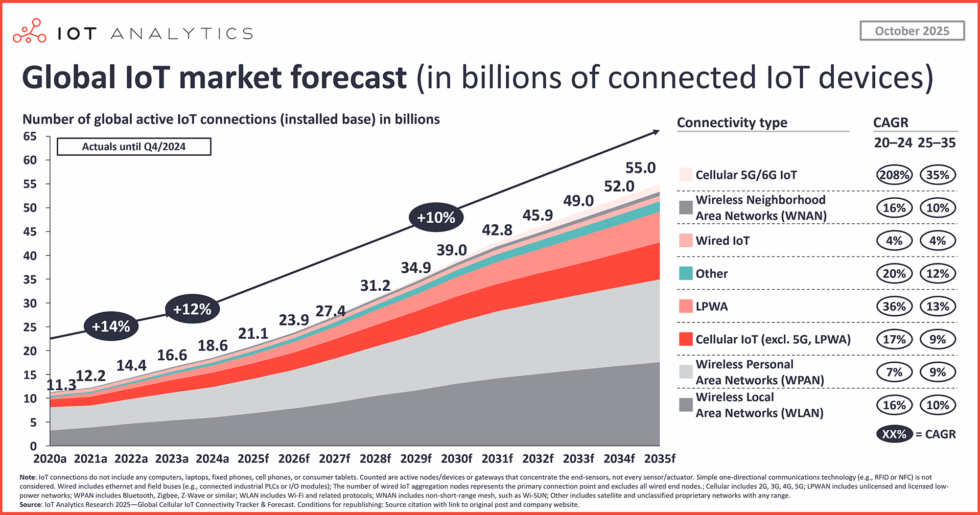

On the device side, IoT Analytics reports that there were about 18.5 billion connected IoT devices in 2024, with forecasts pointing to around 40 billion devices by 2030. That is not just “more hardware”, it is an exponential increase in the signals and context the network can see and respond to.

In simple terms, the internet is expanding along two dimensions at once:

More people are coming online

More devices per person (and per organisation) connected to the network

When those two dynamics overlap, something else tends to appear: new platforms and new services.

Global IoT market forecast (in billions of connected IoT devices)

Source: www.IoT-Analytics.com

The pattern that repeats

Most of the digital platforms we now take for granted did not start out looking like platforms at all. Uber began as a way to get a reliable ride when taxis were scarce. Airbnb helped conference visitors find spare rooms. Shopify gave small merchants a way to sell online without building the rails themselves.

None of them launched as “ecosystems”. They launched as small, useful answers to everyday frustrations. Over time, as that usefulness repeated and spread, something more powerful emerged:

Users returned —> Communities formed —> Entire marketplaces grew around them

Seen from a distance, this growth pattern appears often enough that it almost behaves like a playbook. For SME leaders thinking about digital transformation, it’s a useful way to frame where the next opportunities might sit.

The Platform Playbook

Across industries, most durable platforms tend to evolve through four stages.

Spark —> Retention —> Community —> Monetisation

Step 1: Spark

Every platform begins with a simple reason to try something. Not a complex roadmap or a fully formed business model, just a small moment where a product solves a specific frustration more easily than the alternatives.

The spark might be convenience, access, savings, speed, or just removing friction from something people already do. As connectivity expands into new markets and as more devices come online, these sparks tend to emerge in everyday needs: communication, payments, logistics, healthcare, education, and local services.

At this stage, the goal is not scale. The goal is repeat usefulness.

Step 2: Retention

Trying a product once is easy. Returning to it, building a habit around it, is where real value starts to form. Retention appears when a service becomes part of someone’s routine, not just a one‑off experiment.

Behaviour, not technology, is what ultimately creates defensibility. Global internet users now spend well over six hours a day online on average, which means habits form quickly once a product finds its place in that time. Retention is the moment when a product stops being a novelty and starts becoming infrastructure in people’s lives.

Step 3: Community and network effects

Once retention stabilises, growth often changes character. Platforms stop behaving like standalone products and start behaving like ecosystems.

Users bring other users. Creators bring audiences. Merchants attract customers. At this point, network effects start to appear and growth no longer depends purely on marketing spend. Participation itself becomes the driver of expansion.

For SMEs, this can happen at a smaller, local scale: a niche B2B marketplace in a specific sector, a specialist community of buyers and suppliers, a regional logistics network. The pattern is the same, just tuned to the market you serve.

Step 4: Monetisation

Monetisation tends to work best once the previous stages are in place. Many founders try to reverse this order, optimising pricing and revenue models before behaviour is stable.

The more durable platforms focus first on creating repeated value, then introduce ways to capture a portion of that value. Subscriptions, marketplace fees, transaction margins and services usually present themselves naturally once the platform has become essential to the users it serves.

This moment is different

The “other 2.6 billion” is not just an abstract number. It is a signal about timing and context. The first billion internet users came online into a world of desktop computers, dial‑up connections and scarce services. The next wave arrives at something very different.

Newly connected users will enter a digital environment where:

Smartphones are already dominant

Digital payments are widely available or rapidly expanding

Cloud infrastructure is mature and accessible

AI is embedded in everyday software

Connected devices – from wearables to vehicles to sensors – are everywhere

They will not experience the early internet. They will arrive directly into a multi‑device, AI‑assisted, cloud‑first environment. At the same time, already‑connected consumers and organisations are adding more devices into their daily lives: smart watches and wearables, smart speakers, connected vehicles, sensors in factories and supply chains, and emerging categories like smart glasses.

IDC expects AR/VR headsets and smart glasses shipments to reach around 14.3 million units in 2025, with strong year‑on‑year growth driven in part by devices that bring AI into wearables. That shift turns “screens” into something ambient - always present, always listening, always ready to surface a service.

The next phase of the internet, then, is not just more users; it is rather more users interacting through more devices, in richer contexts, generating more signals. That is fertile ground for entirely new service models, especially for SMEs that can move faster than incumbents and leverage a competitive edge through fast iterative strategies such as the popular OODA loop.

Where SMEs can play

Most SMEs will not build the underlying infrastructure. Hyperscalers, telecom operators and large hardware manufacturers will continue to define that layer. But history shows that the application and service layers on top of infrastructure are where smaller, focused companies often move the fastest.

Three areas stand out for SME leaders and founders.

1. Context‑aware services

As device density increases, more contextual data becomes available; location, behaviour, environment, health metrics, timing, and more. The opportunity lies in turning those signals into practical outcomes for specific customers or sectors.

Examples include proactive healthcare monitoring, risk‑aware insurance products, logistics optimisation, adaptive learning tools and highly personalised local services. Fantastic case examples are companies like Zipline in Rwanda, which demonstrated this pattern early and their drone logistics solved a narrow problem (blood delivery) and became a platform for national medical supply chains.

SME Opportunity: The winning SME doesn’t have to own the data pipeline; it has to understand the context well enough to deliver useful, trusted outcomes.

2. Services for newly connected populations

When new populations come online, they often leapfrog old infrastructure rather than follow the same path. Mobile payments across parts of Africa are the clearest example; entire financial behaviours went straight to mobile, skipping physical banking infrastructure.

Similar patterns are likely in digital identity, financial access for micro‑entrepreneurs, education, healthcare delivery and micro‑commerce.

SME Opportunity: The opportunity is rarely global scale on day one. It is local relevance, delivered quickly, with a deep understanding of culture, regulation and behaviour.

3. Device orchestration

As connected devices multiply, coordination becomes the real problem. Individual devices will get smarter; the gaps will appear in how they work together across homes, workplaces, transport systems, industrial settings and healthcare environments.

Software that helps devices interact coherently, scheduling, permissions, hand‑offs, monitoring and exception handling, becomes increasingly valuable. The more connected systems exist, the greater the need for orchestration layers that make sense of the complexity for the end user.

SME Opportunity: The Connected systems space, that is a natural space for specialist SMEs with domain expertise.

The next phase of the internet

Technology waves rarely feel obvious while they are unfolding. In hindsight, the sequence usually looks familiar:

Infrastructure expands —> Devices spread —> Services emerge

= Platforms follow

The internet’s next phase is likely to follow that same pattern, but this time at a different order of magnitude. We still have around 2.6 billion people to bring online and tens of billions of additional devices to connect.

The companies that build the next generation of platforms will not all start by trying to “build platforms”. They will start by solving small problems that suddenly become possible to solve in this new context.

Final reflection

If there’s one lesson that repeats across markets, technologies and business cycles, it’s that major shifts rarely announce themselves; they start quietly. A new behaviour here, a small use case there, a subtle pattern in how people adopt what’s next and over time, those signals compound.

What begins as a niche service becomes a habit; habits form communities; and communities, when the timing is right, evolve into platforms that reshape entire sectors.

The opportunity around the other 2.6 billion isn’t just about connectivity. It’s about recognising when behaviour starts to change and having the conviction to see in those early moments the seeds of something much larger.

For founders and investors, the game isn't about predicting the next platform; it’s about spotting the spark before the world catches fire. Right now, the oxygen is shifting toward Orlando and Vegas. Between the Microsoft 365 Conference and Google Cloud Next, the next decade of industry standards is being written in real-time. Don’t just watch the headlines, watch for the shift….

🟪 Contributor - Philip Mordecai

Start with a conversation.

We’ll help you see where the next wave of growth is and how to get there.